Security in Payment Switches: Encryption, Tokenization, and Fraud Checks

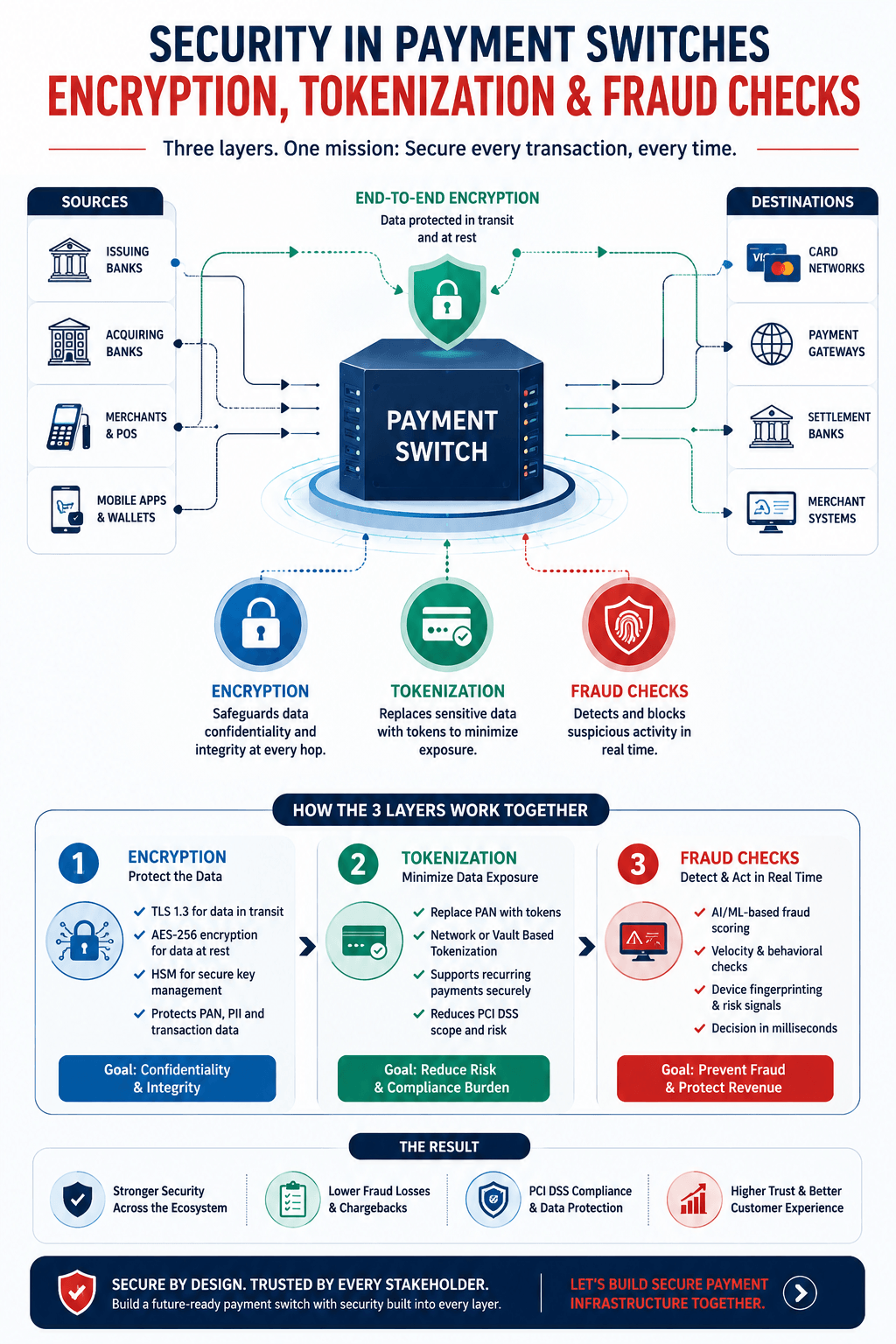

Payment switch security depends on three coordinated layers working together: payment switch encryption that protects data in transit, tokenization in payment processing that eliminates the value of stolen data at rest, and payment switch fraud detection that catches malicious intent before settlement completes. Secure payment switching solutions that treat these as independent checkboxes rather than an integrated security architecture consistently fail at the exact moment a coordinated attack tests all three simultaneously.

Payment switch security sits at the center of one of the most consequential infrastructure decisions in banking and fintech, and most conversations about it stop at the wrong level of detail.

Why payment switch security matters?

Every payment switch vendor will tell you they support encryption. Every payment switch vendor will tell you they support tokenization. Every payment switch vendor will tell you they have fraud detection. These statements are almost universally true and almost universally insufficient, because the question that actually determines whether a payment switch is secure is not whether these three capabilities exist independently, but whether they are architected to work together against the specific attack patterns that target the moment of transition between them.

This is the angle most security reviews miss entirely. Payment switch encryption protects a transaction while it travels. Tokenization in payment processing protects the underlying card data once it arrives. Payment switch fraud detection evaluates whether the transaction itself should be allowed to happen. Each of these operates in a different moment of the transaction lifecycle, and the seams between those moments, the brief windows where data is decrypted for processing, where a token is generated and exchanged, where a fraud score is calculated under a latency budget measured in milliseconds, are where the overwhelming majority of real-world payment switch compromises actually occur.

Understanding payment switch security properly means understanding not just what each layer does, but what happens in the gaps between them, and how secure payment switching solutions are architected to close those gaps rather than simply checking each box independently.

- Layered architecture: Payment transaction security framework design requires encryption, tokenization, and fraud detection to function as a single coordinated system rather than three separate compliance checkboxes.

- Seam vulnerability: The transition points between encrypted transport, token generation, and fraud scoring are where most sophisticated attacks succeed, not within any single security layer operating as designed.

- Latency tension: Real-time fraud detection in payments must complete its analysis within the same millisecond budget that the payment switch uses to route the transaction, creating a genuine architectural tension between security depth and transaction speed.

- Regulatory floor, not ceiling: Payment processing security best practices that only target PCI DSS compliance build to the regulatory minimum rather than to the threat landscape that sophisticated fraud operations actually present in 2026.

What a Payment Switch Actually Does and Why Security Architecture Matters?

A payment switch is the infrastructure layer that routes a transaction between the originating point, such as a card terminal, mobile wallet, or online checkout, and the destination systems, including card networks, issuing banks, and settlement infrastructure. Every transaction passes through this switching layer, which makes it both the most operationally critical and the most attractive target in the entire payment ecosystem.

Banking payment switch architecture has to accomplish something genuinely difficult: process enormous transaction volumes with sub-second latency requirements while maintaining security standards rigorous enough to protect financial data that, if compromised, creates liability extending well beyond the single transaction affected.

This dual requirement, speed and security simultaneously, is the design tension that defines every meaningful decision in payment switch architecture. A switch that prioritizes security checks so thoroughly that it cannot process transactions within acceptable latency windows will fail commercially, regardless of how secure it is. A switch that prioritizes speed at the expense of security depth will eventually fail catastrophically, regardless of how fast it processes transactions until that point.

See Payment Infrastructure Modernization in Action

Discover how Tntra helped a leading financial institution modernize its payment infrastructure for faster transaction processing, improved scalability, and enterprise-grade security.

👉 Read the Case Study:

Future-Proofing a FinTech Provider’s Pay-by-Bank Platform Through Strategic Modernization

Payment Switch Encryption: Protecting Data in Motion

Payment switch encryption is the first and most foundational security layer, responsible for ensuring that transaction data cannot be intercepted and read as it travels between the originating system and the switch, and between the switch and downstream processing systems.

How Encryption Actually Works in Payment Processing?

How encryption protects transactions in payment switches comes down to converting readable payment data into ciphertext that is computationally infeasible to decode without the correct cryptographic key, applied at every point where data moves across a network boundary.

- Transport layer encryption: TLS 1.3 protects data as it moves across network connections between the point of transaction origination, the payment switch, and downstream systems, with TLS 1.3 specifically reducing the handshake overhead that earlier TLS versions introduced, which matters significantly for the latency-sensitive nature of real-time transaction routing.

- Point-to-point encryption: P2PE protects card data from the moment it is captured at the point of interaction through to the point where it reaches a secure decryption environment, ensuring that the merchant or originating system never has access to readable card data at any point in the process.

- End-to-end encryption: Payment gateway encryption methods that implement true end-to-end encryption ensure that data remains encrypted across every hop in the transaction path, rather than being decrypted and re-encrypted at intermediate systems, which is precisely the seam vulnerability that the unique angle of this article addresses.

- Key management infrastructure: Hardware security modules that generate, store, and rotate encryption keys in tamper-resistant hardware environments are essential infrastructure, because encryption is only as strong as the protection around the keys that perform it.

Where Encryption Alone Falls Short

Encryption protects data while it is moving, but encrypted data has to be decrypted at some point for the switch to actually process the transaction, validate the account, and route it to the appropriate destination. That decryption moment, however brief, is a window during which the data exists in readable form somewhere in the system’s memory.

This is precisely why encryption cannot be the only security layer in a payment switch. It is also why understanding tokenization vs encryption in payment processing security as complementary rather than redundant is so important to genuinely secure architecture.

Tokenization in Payment Processing: Removing the Target Entirely

Tokenization in payment processing takes a fundamentally different approach to protecting payment data than encryption does, and understanding that difference is essential to building secure payment switching solutions that actually close the gaps encryption leaves open.

What is the Difference Between Encryption and Tokenization in Payments?

Encryption transforms data into ciphertext that can be mathematically reversed back into the original data if you have the correct key. Tokenization replaces sensitive data with a randomly generated token that has no mathematical relationship to the original data at all. The original data is stored in a highly secured, isolated vault, and the token itself is, on its own, meaningless.

This distinction matters enormously for risk management. If encrypted data is intercepted along with its key, through key compromise, insider threat, or implementation error, the original data can be reconstructed. If a token is intercepted, it is simply a random string with no value to an attacker, because reconstructing the original card data from the token requires access to the secured token vault, which is architected as a completely separate, heavily isolated system.

Payment tokenization solutions therefore solve a specific problem that encryption cannot: they eliminate the value of stolen data even in scenarios where the data itself is somehow exposed, because the token has no exploitable value outside the specific tokenization system that issued it.

- Vault isolation: The token vault that maps tokens back to original card data is isolated from the operational payment switch infrastructure, meaning that even a full compromise of the switching environment does not expose the underlying card data.

- Format-preserving tokens: Tokenization can generate tokens that preserve the format of the original data, such as maintaining the same digit length as a card number, allowing existing systems to process tokens without requiring extensive reengineering.

- Network tokenization: Card network tokenization standards, where Visa, Mastercard, and other networks issue their own tokens tied to specific devices or merchants, add another layer of protection that operates above the merchant or switch level entirely, further limiting the blast radius of any single point of compromise.

- Reduced PCI scope: Because tokenized environments do not store actual card data outside the secured vault, payment processing security best practices increasingly favor tokenization specifically because it dramatically reduces the scope of systems that fall under the most stringent PCI DSS requirements.

Why Tokenization and Encryption Need Each Other?

The critical insight that most security discussions skip is that tokenization and encryption are not competing approaches where you choose one. They protect data during fundamentally different phases of its lifecycle. Encryption protects data in motion, across the network. Tokenization protects data at rest and in use, within the processing environment. A payment switch that implements only one of these has built half a security architecture, regardless of how well that half performs.

Secure transaction routing that genuinely protects payment data uses encryption to move data safely between systems and tokenization to ensure that even systems handling the transaction never need to store or transmit the actual sensitive data at all.

Payment Switch Fraud Detection: Evaluating Intent in Real Time

Encryption and tokenization protect data. Payment switch fraud detection protects against the transaction itself being malicious, which is a categorically different and arguably more difficult problem, because fraud detection has to make a judgment call about intent within an extremely tight latency budget.

How Payment Switches Detect Fraudulent Transactions?

How do payment switches detect fraudulent transactions comes down to analyzing multiple risk signals simultaneously and generating a risk score that determines whether a transaction proceeds, gets flagged for additional verification, or gets blocked outright, all within the same processing window the switch uses to route the transaction in the first place.

- Behavioral baseline analysis: Machine learning models compare each transaction against the established behavioral pattern of the specific account, flagging transactions that deviate meaningfully from that account’s typical spending velocity, geography, merchant category, or time-of-day pattern.

- Velocity checks: Real-time fraud detection in payments monitors transaction frequency and cumulative value across short time windows to catch the rapid sequential transactions that characterize card testing attacks and account takeover exploitation.

- Device and network fingerprinting: Analysis of the originating device, IP address, and network characteristics identifies when a transaction is originating from an environment inconsistent with the account holder’s established usage pattern.

- Network-level pattern sharing: Modern fraud prevention in digital payments increasingly relies on consortium data sharing, where fraud signals identified across multiple institutions and payment switches inform risk scoring in real time, catching fraud patterns that a single institution’s isolated data would never reveal in time to act.

The Latency Constraint that Defines Fraud Detection Architecture

This is where the unique architectural tension of payment switch security becomes most acute. Fraud detection models, particularly the most sophisticated machine learning approaches, can take meaningful computational time to evaluate a transaction thoroughly. Payment switches operate under latency budgets that are frequently measured in tens of milliseconds for the entire transaction, including authentication, encryption and decryption overhead, fraud scoring, and routing.

This means payment switch fraud detection architecture has to be deliberately designed around tiered evaluation: lightweight rule-based checks that execute almost instantly to catch obvious fraud patterns, combined with more sophisticated machine learning risk scoring that operates within a carefully bounded time allowance, with a clear fallback path for transactions that cannot be fully evaluated within the available window.

Switches that do not architect for this tension end up making a forced choice between unacceptable transaction latency and inadequate fraud screening, and the switches that fail in production are almost always the ones that did not design explicitly for this trade-off from the beginning.

Why Payment Switch Security is Important for Banks and Fintech Companies?

Why is payment switch security important for banks and fintech companies goes beyond regulatory compliance, though compliance is certainly part of the answer. The payment switch is the single point through which the highest volume of an institution’s most sensitive financial data flows, which makes it simultaneously the most operationally critical system and the highest value target for sophisticated attackers.

A security failure at the payment switch level has a different character than a security failure almost anywhere else in financial infrastructure. It is not contained to one customer, one account, or one product line. It potentially exposes the transaction data flowing through the entire institution at the moment of compromise, which is precisely why regulatory frameworks, card network requirements, and institutional risk management all treat payment switch security as a foundational priority rather than a feature to be added later.

What is PCI DSS Compliance for Payment Systems?

What is PCI DSS compliance for payment systems is the baseline regulatory framework that governs how organizations handling payment card data must protect that data, covering requirements across network security, access control, encryption standards, vulnerability management, and ongoing monitoring.

PCI DSS compliance is necessary but should be understood explicitly as a floor rather than a ceiling. The standard defines minimum acceptable practices, and organizations that build their security architecture to exactly meet PCI DSS requirements and no further are building to satisfy auditors rather than to withstand the sophisticated, continuously evolving attack techniques that target payment infrastructure specifically because of the value concentrated there.

Secure payment switching solutions that genuinely protect transaction data treat PCI DSS as the starting point for a security architecture, then layer the coordinated encryption, tokenization, and fraud detection design discussed throughout this article on top of that baseline, specifically addressing the seam vulnerabilities between security layers that compliance checklists do not typically evaluate.

Building Payment Switch Security Architecture for Real-Time Transaction Processing

Payment switch security architecture for real-time transaction processing that genuinely closes the gaps between encryption, tokenization, and fraud detection requires treating these three capabilities as a single integrated design problem from the earliest architectural decisions, rather than implementing each independently and integrating them afterward.

- Unified security data layer: Encryption key management, tokenization vault access, and fraud detection signal processing should draw from a coordinated security data layer rather than operating as isolated systems that each maintain their own state and context.

- Minimized decryption windows: Architecture should minimize the time and scope during which transaction data exists in decrypted form, processing as much risk evaluation as possible on tokenized or encrypted representations of the data rather than requiring full decryption for every check.

- Coordinated incident response: When fraud detection flags a transaction, the response needs to coordinate across the encryption and tokenization layers as well, ensuring that flagged transaction data is handled with appropriate additional protection rather than following the standard processing path.

- Continuous architecture review: Payment fraud prevention solutions and the broader security architecture need ongoing review against an evolving threat landscape, because the attack techniques that targeted payment switches three years ago are meaningfully different from the techniques being deployed against payment infrastructure today.

How Tntra Builds Secure Payment Switch Infrastructure?

At Tntra, our fintech practices and payment switch development company capability is built around the principle this article describes: encryption, tokenization, and fraud detection have to be architected as one coordinated security system, not three independent compliance checkboxes.

Our fintech software development company practice delivers fintech payment infrastructure solutions that close the seam vulnerabilities between security layers, with payment security consulting services that evaluate not just whether each security control exists, but whether they work together against the specific attack patterns that target the transition points between them.

Through our transaction monitoring systems and fraud detection and risk management capabilities, we help banks and fintech companies build digital payment solutions and banking software development services that meet the latency demands of real-time transaction processing without compromising the security depth that modern payment infrastructure genuinely requires.

Build a Secure, Future-Ready Payment Switch with Tntra

From end-to-end encryption and PCI DSS compliance to real-time fraud detection and high-performance payment switching, Tntra helps banks, FinTechs, and payment providers build secure, scalable payment infrastructure designed for modern digital payments.

👉 Talk to Our Payment Switch Experts: Contact us now!

FAQs

What is a Payment Switch in Banking?

A payment switch is the infrastructure layer that routes transactions between originating systems, such as card terminals or mobile wallets, and destination systems including card networks and issuing banks. It processes authentication, security checks, and routing logic for every transaction.

How Does Encryption Work in Payment Processing?

Encryption converts payment data into unreadable ciphertext using cryptographic algorithms as it travels across network connections. This protects sensitive information from interception, with the data only readable by systems that possess the correct decryption key.

Is Tokenization More Secure Than Encryption?

Tokenization and encryption protect different stages of the payment data lifecycle rather than competing with each other. Tokenization provides stronger protection for stored and processed data because tokens have no exploitable value outside their secure vault, while encryption protects data during transmission across networks.

How Do Banks Prevent Fraud in Digital Transactions?

Banks prevent fraud using multiple security layers, including behavioral analysis, transaction velocity monitoring, device and network fingerprinting, and consortium data sharing across financial institutions. These systems generate real-time risk scores to determine whether a transaction should be approved, challenged with additional verification, or blocked.

What are the Key Security Layers in a Payment Switch?

The primary security layers in a payment switch include encryption for protecting data in transit, tokenization for securing stored and processed data, and fraud detection for evaluating transaction risk in real time. Strong payment security depends on how effectively these technologies work together.

What is PCI DSS Compliance for Payment Systems?

PCI DSS (Payment Card Industry Data Security Standard) is the security framework that defines the minimum requirements for organizations handling payment card data. It covers network security, access controls, encryption, vulnerability management, and continuous monitoring, serving as a baseline for protecting payment systems against cyber threats.

{kind=link}

{kind=link}