How to Build a Secure and Scalable FinTech Platform Architecture (AI, Payments, Cloud)?

This article explains how to build secure and scalable fintech systems through strong architecture, payment infrastructure, AI integration, cloud-native engineering, and platform-led development. It covers scalable fintech platform architecture, fintech microservices architecture, cloud-native infrastructure, multi-region deployment, payment processing resilience, digital banking systems, payment orchestration, security best practices, PCI DSS readiness, fintech scalability challenges, and the role of AI in modern financial ecosystems.

The article also explores how enterprise innovation infrastructure supports long-term fintech growth and explains the connection between platform strategy and T(u)LIP, helping organizations move from fintech ideas to structured, future-ready execution. Continue reading to learn more.

Why Modern FinTech Platform Architecture Matters?

Building a modern FinTech product feels exciting in the early stages. But real challenges begin when questions around real-time transactions, security, and scalability emerge.

How will transactions move in real time?

How will sensitive financial data stay protected?

How will the system scale when usage spikes across onboarding, lending, or payments?

These are the foundations of a strong fintech platform architecture, and they define whether your product becomes a secure fintech platform or struggles under pressure.

The reality is simple: great FinTech companies are not built on features alone. They are built on trust, resilience, and adaptability. That is why every secure fintech platform must also be a scalable fintech platform, supported by a strong fintech software architecture that evolves with the business.

Today’s expectations go even further. Customers expect instant payments, seamless onboarding, intelligent insights, and always-on reliability. This has pushed organisations to adopt a cloud-based fintech platform, powered by AI-powered fintech platform capabilities and modern payment platform architecture strategies.

Why FinTech Platform Architecture is a Strategic Advantage?

A FinTech platform operates in one of the most sensitive digital environments. Money flows through the system. Personal identity flows through the system. Compliance defines how the system behaves.

This is why FinTech platform architecture is not just engineering—it is business strategy.

A well-designed enterprise FinTech platform enables:

- Expansion into multiple financial products

- Seamless integration with core banking systems

- Faster innovation using open banking APIs

- Growth into embedded finance platforms

Without strong architecture, scaling becomes painful, compliance becomes risky, and innovation slows down.

Start with the Right FinTech System Architecture Design before You Write Code

The biggest mistake teams make is treating architecture as something they’ll “figure out later.” Fintech platform architecture solutions demand intentional design from day one, because the cost of retrofitting a monolithic structure into a distributed one — while processing live financial transactions — is enormous. Think of it like trying to rewire a building’s electrical system while people are working inside.

Scalable fintech platform architecture begins with a clear answer to one question: what are the core domains of this system?

- Payments

- Identity

- Compliance

- Notifications

- Ledger management

- Fraud detection

Each of these is a distinct domain with its own data model, scaling profile, and failure modes. When you treat them as separate concerns from the start, you create room to scale each independently.

A strong fintech system architecture design should also account for the difference between what the platform does today and what it may need to do in 18 months. A platform serving 10,000 users in India is fundamentally different from one serving 500,000 users across India, Southeast Asia, Europe, and the Middle East.

This is the foundation of fintech platform architecture for global markets and one of the core principles behind how to design scalable fintech platform for global users without constant rebuilding.

The Core Layers of a Secure and Scalable FinTech Platform

A modern digital banking platform architecture is built as a layered system. Each layer has a clear role but must work seamlessly with others.

1. Experience Layer (Customer Interaction Layer)

This includes:

- Mobile banking apps

- Web platforms

- Merchant dashboards

This layer handles onboarding, payments, account access, and support experiences. It must remain lightweight and responsive.

2. Domain Services Layer (Business Logic Layer)

This is where the core financial services live:

- Identity and KYC

- Payments and transfers

- Lending and underwriting

- Wallets and cards

- Fraud detection

Most modern systems implement this using microservices architecture for fintech, allowing each service to scale independently.

3. Integration Layer (API & Partner Ecosystem Layer)

FinTech platforms rarely operate alone. They integrate with:

- Banks

- Payment processors

- AML/KYC providers

- Credit bureaus

This is where an API-first fintech platform becomes essential. APIs enable flexibility, scalability, and faster partner onboarding.

4. Data Layer (Financial & Analytical Data Systems)

This layer manages:

- Transaction records

- Ledger systems

- Customer data

- Analytics pipelines

A strong fintech data architecture ensures:

- Data consistency

- Auditability

- Regulatory compliance

5. Control Layer (Security, Compliance, Observability)

This includes:

- Identity and access management

- Encryption and key management

- Monitoring and logging

It aligns with fintech security best practices and ensures adherence to PCI DSS compliance fintech standards.

Choosing the Right Architecture for FinTech Platforms

There is no single template that fits every FinTech business. The right fintech platform architecture depends on several factors:

- Product scope

- Transaction volumes

- Compliance exposure

- Integration complexity

- Organisational maturity

Still, some architectural patterns consistently work well.

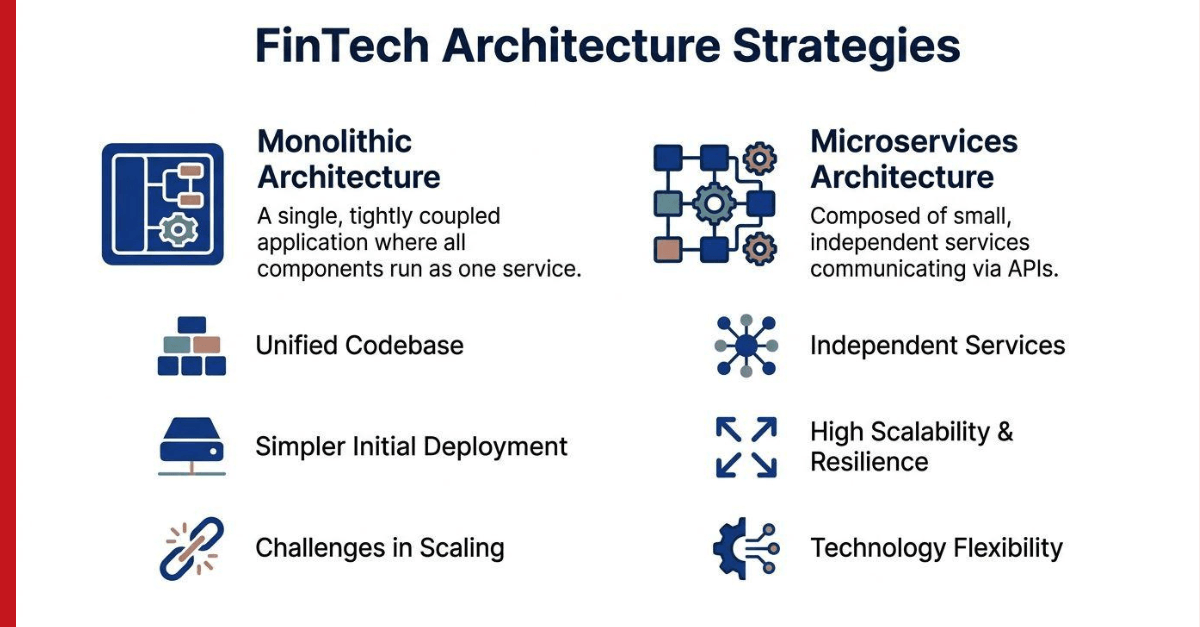

1. Modular Monolith (Best for Early-Stage Platforms)

Many early-stage teams begin with a modular monolith. This is often a healthy choice when:

- The product scope is narrow

- The engineering team is small

- Coordination across teams is critical

A modular monolith helps teams:

- Move faster with focused development

- Maintain clear code boundaries across domains

However, discipline is key.

If the system becomes tightly coupled, scaling the platform can quickly become difficult.

2. Microservices Architecture for FinTech (Scaling Stage)

As products grow, teams often transition to microservices architecture for fintech.

This becomes useful when different business domains need to scale independently, such as:

- Payments

- KYC and onboarding

- Notifications

- Reporting

- Ledger operations

- Fraud detection

Each of these areas may have different:

- Performance requirements

- Reliability expectations

Independent services help manage this complexity effectively.

3. API-First FinTech Platform (Integration & Expansion)

As the business expands, adopting an API-first fintech platform becomes increasingly important.

APIs enable:

- Clean connections between internal services

- Seamless partner integrations

- Support for embedded finance use cases

- Expansion into external distribution channels

Well-designed APIs also improve:

- Consistency across systems

- Governance and control

- Reusability across teams

4. Event-Driven Architecture for High-Volume Systems

For high-volume and high-velocity environments, event-driven architecture fintech patterns provide strong advantages.

These are especially useful for:

- Payments

- Balance updates

- Transaction notifications

- Fraud signals

- Settlement workflows

- Reconciliation events

Event-driven systems support:

- Asynchronous processing

- Faster responsiveness

- Better system resilience

- Easier extensibility

They also improve auditability when event histories are properly maintained.

5. Hybrid Architecture (What Most Successful Platforms Use)

In reality, most successful FinTech platforms combine multiple approaches rather than choosing just one.

For example:

- A central ledger may require strong consistency

- A notification system may be event-driven

- A rules engine may expose APIs

- A fraud pipeline may use streaming

- A reporting service may operate independently

The architecture becomes stronger when:

- Each component is designed based on its role

- Systems are loosely coupled but well integrated

- Performance and reliability needs are handled separately

Key Takeaway

The best architecture is not about choosing one pattern.

It’s about combining the right approaches to build a scalable fintech platform that is:

- Flexible

- Resilient

- Easy to extend

- Aligned with business growth

Why FinTech Microservices Architecture Powers Global Scale?

Fintech microservices architecture has become an industry standard for a reason. When you decompose a platform into independently deployable services, you gain the ability to scale components based on real demand patterns.

Your payment processing service might need 10x more resources during peak transaction windows, while your analytics or reporting layer remains relatively idle. With a monolith, you’d scale everything together. With microservices, you scale precisely.

But microservices also introduce complexity:

- Service-to-service communication

- Distributed tracing

- Cross-service data consistency

- Independent deployment pipelines

- Observability and monitoring

These are the realities every fintech platform architecture for global markets must handle.

The teams that do this successfully follow a few principles consistently:

Service Ownership and API Isolation

Each service owns its own data. No shared databases. Services expose state through APIs aligned with fintech API architecture best practices.

In fintech systems, APIs are not just interfaces — they are contracts.

That means APIs should:

- Be versioned from day one

- Support backward compatibility

- Use strong authentication and authorization

- Include detailed documentation

- Support auditability and traceability

A strong API layer also enables more modular fintech software development solutions, allowing teams to launch new products faster using reusable building blocks instead of rebuilding functionality repeatedly.

This composability is one of the defining characteristics of the best architecture for fintech platforms handling millions of transactions.

Build Cloud-Native Cloud Architecture for FinTech Platforms

Modern cloud architecture for fintech platforms has evolved far beyond basic infrastructure migration. Today’s leading fintech software development services are designed cloud-native from the ground up.

That means:

- Infrastructure-as-code

- Container orchestration

- Auto-scaling services

- Managed databases

- Global CDN distribution

- Automated disaster recovery

- Observability-first infrastructure

Cloud-native application development gives fintech teams the flexibility to deploy rapidly, recover faster, and scale globally without excessive operational complexity.

A major advantage of this model is the ability to build high availability fintech systems capable of surviving infrastructure failures without disrupting user experiences.

Designing a Multi-Region FinTech Deployment Strategy

This is where global fintech infrastructure solutions become truly complex.

Operating across multiple countries introduces competing architectural requirements:

- Data residency regulations

- Regional compliance mandates

- Low-latency transaction processing

- Disaster recovery expectations

- Currency and payment rail variations

A robust multi-region fintech deployment strategy generally relies on active-active or active-passive regional deployments.

Active-Active Architecture

Ideal for:

- Read-heavy workloads

- Customer dashboards

- Reporting systems

- Content delivery

Multiple regions serve traffic simultaneously for low latency and redundancy.

Active-Passive Architecture

Often preferred for:

- Payment processing

- Transaction ledgers

- Settlement systems

These workloads require stronger consistency guarantees, making synchronization across distributed regions more challenging.

This is where distributed systems in fintech become essential. Teams must carefully balance consistency, availability, and performance — especially for financial data integrity.

Architecting Scalable Payment Processing Systems

At the heart of every global fintech platform sits one critical component: payments.

Building scalable payment processing systems is about far more than handling large transaction volumes.

Modern payment systems must support:

- Idempotent transaction processing

- Event-driven recovery

- Ledger consistency

- Fraud monitoring

- Retry management

- Failure isolation

- Auditability

This is the foundation of how to build secure and scalable payment systems globally.

Why Global Payment Gateway Architecture Matters?

Different markets rely on different payment rails:

- UPI in India

- SEPA in Europe

- ACH in the United States

- PromptPay in Thailand

A strong global payment gateway architecture introduces abstraction layers that allow new payment methods and providers to be integrated without rewriting the core platform.

This is why mature payment system development solutions rely on provider-agnostic orchestration models.

The result:

- Faster regional expansion

- Lower vendor lock-in

- Improved resilience

- Better failover handling

Compliance must be Built into the Architecture

One of the most expensive fintech mistakes is treating compliance as a post-development activity.

True fintech compliance and scalability solutions only work when compliance becomes part of the architectural foundation.

Key Compliance Architecture Components

Immutable Audit Logs

Every financial event should be recorded in append-only logs for traceability and regulatory reporting.

Role-Based Access Controls

Frameworks like GDPR, PCI-DSS, and RBI compliance require strict control over who accesses sensitive financial data.

Jurisdiction-Based Rule Engines

A platform entering multiple countries must support region-specific:

- KYC workflows

- AML policies

- Tax logic

- Reporting rules

This is essential for building fintech platform architecture for multi-country compliance without duplicating infrastructure.

Many fintech platform scalability challenges appear at the exact intersection of rapid growth and increasing compliance obligations.

This is where strong enterprise platform engineering services become strategically important.

Building Resilient and High Availability FinTech Systems

Reliable FinTech infrastructure is intentionally engineered.

The best high availability FinTech systems consistently implement:

Circuit Breakers and Graceful Degradation

If a dependency fails, the platform should continue operating safely rather than causing cascading outages.

Chaos Engineering

Controlled failure testing helps teams understand how systems behave under real stress conditions.

SLO-Driven Engineering

Clear service level objectives create organizational accountability around reliability and uptime.

These fintech practices are not just technical disciplines — they shape company culture.

The Role of AI in Modern FinTech Platforms

AI now has a meaningful role in platform design, but the strongest implementations are practical rather than decorative. An AI-powered fintech platform supports better decisions, better detection, better personalization, and better operational efficiency when AI is connected to real workflows and governed carefully.

The role of AI in FinTech platform scalability shows up in several ways. AI can help automate fraud detection, improve underwriting signals, support risk scoring, personalize product recommendations, classify support cases, summarize compliance review data, detect anomalies in transaction behavior, and improve operational forecasting. In customer-facing environments, AI can help deliver faster assistance and smoother journeys. In internal environments, it can support analysts, ops teams, and compliance reviewers with higher-quality context.

An AI-first FinTech architecture treats intelligence as a platform capability, not as a disconnected experiment. That means designing pipelines for feature generation, event ingestion, model serving, observability, feedback loops, governance, and access control. It also means understanding where AI should influence decisions and where human review should remain central.

For example, a lending platform may use AI for document classification, affordability pattern analysis, and preliminary risk insights. A payments platform may use AI to enhance fraud screening and merchant anomaly detection. A digital banking experience may use AI to create personalized financial nudges, spending summaries, and support interactions. Across all of these, the architecture must preserve explainability, accountability, and safe escalation paths.

An AI-first enterprise platform also needs operational discipline. Model performance can drift. Risk patterns can change. Regulatory expectations can evolve. Teams need monitoring for model behavior, clear ownership for approvals, and strong controls over training data, inference logic, and production release practices.

When AI is introduced in this grounded way, it improves the platform without weakening trust. That matters enormously in FinTech.

What Digital Transformation in FinTech Actually Requires?

The phrase digital transformation in fintech gets overused, but at its core it means this:

Financial institutions are being asked to deliver experiences that legacy systems were never designed to support.

The transformation is both technical and organizational.

Teams building modern FinTech practices need:

- Product managers who understand regulation

- Engineers experienced in distributed systems

- Security-first infrastructure teams

- Designers who understand financial user behavior

The strongest product development services teams now focus heavily on continuous discovery and incremental delivery rather than large, risky releases.

They instrument everything:

- Transaction flows

- Drop-off points

- Failure patterns

- Latency metrics

- Conversion bottlenecks

This operational visibility is critical for maintaining high availability FinTech systems at scale.

Digital Banking and Enterprise FinTech Platform Design

Many FinTech businesses eventually become broader than their original product. A payment company adds wallets. A lending company expands into embedded finance. A neobank adds card programs, rewards, wealth features, or SME services. This is where digital banking platform architecture and enterprise FinTech platform thinking become increasingly relevant.

A strong enterprise-ready platform supports multiple journeys without collapsing under its own weight. It can serve customer accounts, transaction management, card controls, notifications, compliance rules, lending workflows, analytics, and partner ecosystems without forcing every feature into one rigid system. Platform leaders think in terms of capability layers, reusable services, and product extensibility.

This is where platform-led FinTech development creates long-term value. Instead of building every new feature as an isolated project, organisations invest in common rails: identity, payments, ledgering, risk, alerts, reporting, workflow orchestration, partner APIs, and governance. New products can then be launched faster because the platform already carries the heavy structural work.

For a growing FinTech company, that is a major strategic shift. The conversation moves from shipping one more product to creating a system that keeps making product creation easier.

Innovation Infrastructure and the Link to T(u)LIP

FinTech platforms rarely fail because the market has no demand for innovation. They struggle when ideas, architecture choices, engineering execution, governance, and operational learning remain disconnected. That is why modern FinTech growth increasingly depends on internal innovation infrastructure.

An enterprise innovation platform helps organisations manage the journey from idea discovery to platform execution with more clarity. In FinTech, this becomes especially useful because innovation often touches regulated workflows, payment complexity, security controls, and cross-functional approvals. Teams need a structured way to evaluate what to build, how to prioritize it, what risks it introduces, and how it connects to platform strategy.

This is where a platform like T(u)LIP can play an important role. As part of a broader innovation system, T(u)LIP supports the lifecycle thinking required to turn promising ideas into structured initiatives, align innovation with architecture decisions, and keep cross-functional progress visible. In a FinTech context, that kind of platform support becomes valuable when organisations are balancing product expansion, AI adoption, compliance expectations, partner ecosystems, and platform modernization at the same time.

Instead of treating innovation as scattered brainstorming, a platform-led approach helps connect ideas to execution pathways, technical ownership, and business outcomes. That becomes very powerful in fast-moving financial environments.

Think in Platforms, Not Just Products

The most successful fintech companies eventually stop thinking in isolated products and start thinking in platforms.

Platform-first organizations build reusable capabilities that support:

- Multiple products

- Regional expansion

- Partner ecosystems

- Third-party integrations

- Faster experimentation

This mindset influences:

- Fintech microservices architecture

- API strategy

- Data ownership models

- Shared infrastructure design

It is also what enables scalable cloud infrastructure for fintech startups and enterprises to evolve efficiently over time.

The companies that invest early in global fintech infrastructure solutions tend to become more resilient, adaptable, and operationally efficient as they grow.

Building global fintech infrastructure is hard. But when architecture, resilience, compliance, and scalability are designed intentionally from the start, what gets built isn’t just software — it’s the foundation for how people interact with money globally.

Working with the Right Engineering Partner

Many FinTech businesses reach a point where architecture quality becomes inseparable from business quality. Product ambitions grow faster than internal bandwidth. Compliance pressure increases. Integrations multiply. Payment volumes rise. AI opportunities emerge. At that stage, working with the right fintech software development company can significantly shape the future of the platform.

A strong engineering partner brings more than development capacity. They bring architectural thinking, domain sensitivity, platform discipline, cloud experience, security maturity, and the ability to translate business priorities into technical systems. They understand that a fintech solution needs trust, performance, resilience, and clarity across product, engineering, and operations.

The best partners also help teams improve internal fintech practices. They support architecture reviews, domain modeling, release discipline, API strategy, observability, cloud modernization, security controls, platform engineering workflows, and AI integration patterns that suit real enterprise needs.

Ready to Build a FinTech Platform that Actually Scales?

At Tntra, we help companies build fintech platform solutions engineered for resilience, compliance, and global scale from day one.

Whether you’re launching a new payment ecosystem, modernizing legacy banking infrastructure, or expanding internationally, our team helps architect platforms that can grow without compromising reliability.

A strong fintech software development company helps:

- Build scalable systems

- Apply strong fintech practices

- Deliver long-term fintech solutions

Schedule a call with us today!

FAQs: FinTech Platform Architecture, Security, and Scalability

What is FinTech Platform Architecture?

FinTech platform architecture is the structural design behind a financial product, including how payments, data, security, compliance, APIs, and user experiences work together. It shapes how the fintech platform architecture performs, scales, integrates, and stays reliable as the business grows.

What is scalable FinTech Architecture and why is it important?

Scalable fintech platform architecture refers to designing fintech systems that can handle increasing transaction volumes, users, and geographic expansion without compromising performance, security, or reliability. It is important because fintech platforms must support rapid growth, compliance requirements, and real-time financial operations globally.

How Do You Build a Secure FinTech Application?

You build a secure fintech application by embedding security into every layer, from identity controls and encryption to audit trails, secure APIs, compliance workflows, and monitoring. Strong architecture, careful data handling, and payment-grade practices help create a secure fintech platform from day one.

What Architecture is Best for Payment Systems?

The best architecture for payment systems usually combines:

- API-first design

- Strong transaction orchestration

- Event-driven processing

- A reliable ledger layer

This approach strengthens payment platform architecture, enabling real-time flows, traceability, resilience, and scalability.

How Does AI Improve FinTech Platforms?

AI improves fintech platforms by helping with:

- Fraud detection

- Risk scoring

- Customer insights

- Support automation

- Smarter decision-making

It enhances efficiency by turning large volumes of data into actionable insights, supporting an AI-powered fintech platform.

What is Scalable Infrastructure in FinTech?

Scalable infrastructure in fintech is a foundation that can handle:

- Growing users

- Increasing transaction volumes

- Expanding product lines

- Complex integrations

It typically includes:

- Cloud services

- Modular systems

- Observability tools

- Automation

This enables a scalable fintech platform without performance loss.

What are the Security Standards for FinTech Platforms?

Security standards for fintech platforms typically include:

- PCI DSS for payment data

- Strong encryption practices

- Secure access controls

- Audit logging

- Data protection measures

- Compliance-aware development

These standards ensure strong fintech platform security architecture and protect transactions, users, and system integrity.

{kind=link}